2009年12月6日日曜日

2009年11月27日金曜日

ドバイ

リスクを見落としていた?楽観視し過ぎた?いいえ。

事態が大きすぎて誰も処理したく無いだけでしょうね。

Dubai Debt May Be Higher Than $80 Billion, UBS Analysts Say

By Anthony DiPaola and Chris Bourke

Nov. 27 (Bloomberg) -- Dubai, the Persian Gulf emirate whose state-run companies are seeking to defer debt payments, may owe more than the $80 billion to $90 billion in liabilities assumed by investors, UBS AG analysts said in a note.

“Perhaps Dubai’s debt includes sizeable off-balance sheet liabilities that imply a total debt burden well above the $80 billion to $90 billion markets have estimated so far,” real estate analyst Saud Masud wrote in a note yesterday. “This could imply that the debt issued by Dubai in recent weeks is insufficient to meet upcoming redemptions.”

Dubai, which has said it will raise as much as $20 billion selling bonds to repay borrowings, said on Nov. 25 that state- run Dubai World, with $59 billion of liabilities, would ask creditors for a “standstill” agreement as it negotiates to extend debt maturities.

The request to delay debt repayment “came as a major shock” to investors, Masud and analyst Reinhard Cluse wrote in the note. Dubai World property unit Nakheel PJSC has $3.52 billion of Islamic bonds due Dec. 14.

Dubai accumulated $80 billion of debt by expanding in banking, real estate and transportation before credit markets seized up last year. The second biggest of seven sheikhdoms that make up the United Arab Emirates formed a fund to help reorganize state firms and sold $10 billion in bonds to the national central bank in February.

It borrowed an additional $5 billion from Abu Dhabi government-controlled banks Nov. 25, half the $10 billion in bonds that Dubai ruler Sheikh Mohammed Bin Rashid Al-Maktoum said he planned to raise by yearend.

Repayment Delay

Seeking a repayment delay may indicate that Abu Dhabi, the U.A.E.’s largest sheikhdom, may not want to support Dubai further financially until the smaller emirates addresses internal problems at government-run companies, UBS wrote.

The request could also suggest that Abu Dhabi and Dubai have decided to seek to bolster long-term confidence in the market by forcing weaker parts of government businesses to take responsibility for bad decisions, Masud and Cluse wrote. That could involve defaults at some Dubai firms, they said.

Dubai property developers may be liable for an estimated $11 billion required to build 40,000 homes that they have started, said Masud in an interview yesterday. That amount represents the off-balance sheet cost, or “funding gap” required to complete and hand over the properties, on which investors are now defaulting, by the end of 2010.

Nakheel’s share of that funding gap is about $2 billion, estimated Masud. Around half of the investors in the 40,000 unfinished homes may default by the end of next year, he said.

事態が大きすぎて誰も処理したく無いだけでしょうね。

Dubai Debt May Be Higher Than $80 Billion, UBS Analysts Say

By Anthony DiPaola and Chris Bourke

Nov. 27 (Bloomberg) -- Dubai, the Persian Gulf emirate whose state-run companies are seeking to defer debt payments, may owe more than the $80 billion to $90 billion in liabilities assumed by investors, UBS AG analysts said in a note.

“Perhaps Dubai’s debt includes sizeable off-balance sheet liabilities that imply a total debt burden well above the $80 billion to $90 billion markets have estimated so far,” real estate analyst Saud Masud wrote in a note yesterday. “This could imply that the debt issued by Dubai in recent weeks is insufficient to meet upcoming redemptions.”

Dubai, which has said it will raise as much as $20 billion selling bonds to repay borrowings, said on Nov. 25 that state- run Dubai World, with $59 billion of liabilities, would ask creditors for a “standstill” agreement as it negotiates to extend debt maturities.

The request to delay debt repayment “came as a major shock” to investors, Masud and analyst Reinhard Cluse wrote in the note. Dubai World property unit Nakheel PJSC has $3.52 billion of Islamic bonds due Dec. 14.

Dubai accumulated $80 billion of debt by expanding in banking, real estate and transportation before credit markets seized up last year. The second biggest of seven sheikhdoms that make up the United Arab Emirates formed a fund to help reorganize state firms and sold $10 billion in bonds to the national central bank in February.

It borrowed an additional $5 billion from Abu Dhabi government-controlled banks Nov. 25, half the $10 billion in bonds that Dubai ruler Sheikh Mohammed Bin Rashid Al-Maktoum said he planned to raise by yearend.

Repayment Delay

Seeking a repayment delay may indicate that Abu Dhabi, the U.A.E.’s largest sheikhdom, may not want to support Dubai further financially until the smaller emirates addresses internal problems at government-run companies, UBS wrote.

The request could also suggest that Abu Dhabi and Dubai have decided to seek to bolster long-term confidence in the market by forcing weaker parts of government businesses to take responsibility for bad decisions, Masud and Cluse wrote. That could involve defaults at some Dubai firms, they said.

Dubai property developers may be liable for an estimated $11 billion required to build 40,000 homes that they have started, said Masud in an interview yesterday. That amount represents the off-balance sheet cost, or “funding gap” required to complete and hand over the properties, on which investors are now defaulting, by the end of 2010.

Nakheel’s share of that funding gap is about $2 billion, estimated Masud. Around half of the investors in the 40,000 unfinished homes may default by the end of next year, he said.

2009年10月30日金曜日

2009年7月3日金曜日

2009年5月28日木曜日

黄海緊張

【ソウル=水沼啓子】北朝鮮が2回目の核実験や短距離ミサイルの発射に加えて韓国との軍事衝突も辞さないとする姿勢を示したことを受けて、米韓連合軍司令部は28日、北朝鮮情報の監視態勢を上から2番目のレベル2に1段階引き上げた。

これにより偵察機による情報収集や分析要員の増員など北朝鮮を監視する態勢が強化され、南北間の緊張が高まっている。

韓国国防省報道官によると、28日午前7時15分に引き上げた。監視レベルは5段階で、レベル2は軍事的緊張が高まった場合に適用される。北朝鮮が1回目 の核実験を実施した2006年10月以来のことで、今回で5回目となる。いちばん高い「1」はこれまで発令されたことがない。

報道官は「北朝鮮の挑発を抑止するため、軍事的な態勢に万全を期している。挑発的な行為は決して容認できないことであり、断固として強力に対応する」と述べた。

この措置に先立ち、韓国国防省は25日、北朝鮮の核実験実施が明らかになった直後、全軍に警戒態勢を強化し、軍事境界線や黄海上での北朝鮮による軍事的挑発に備えるように指示を出している。

一方、北朝鮮は27日、韓国が大量破壊兵器拡散防止構想(PSI)への正式参加を決めたことを「宣戦布告と見なす」とし軍事衝突の可能性を示唆する声明を発表した。とくに、声明では黄海上にある韓国領の延坪島など5島の法的地位や周辺海域での米韓艦船などの安全な航海を担保できないと警告した。

北朝鮮は今年1月から、1953年に設定された黄海上の軍事境界線「北方限界線(NLL)」を認めないという立場を強調。北朝鮮が海岸部に配備している火砲の訓練回数が増加するなど、黄海上での緊張が高まっていた。こうした北の動きに対し、韓国の李相喜国防相は2月に開かれた国会で、黄海で北朝鮮が韓国側の船舶に先制攻撃を加えれば、砲撃した火砲や誘導ミサイルの発射地点に対して反撃を加えると述べるなど、南北間で“前哨戦”がエスカレートしていた。

黄海上では1999年6月と2002年6月の2回、激しい軍事衝突があった。この時期はワタリガニ漁の最盛期で、この海域では南北それぞれ大量の漁船が操業している。いずれの衝突も漁船を監視する名目で、北朝鮮の警備艇が南下し、韓国の高速艇を先制攻撃したのが原因だ。

韓国メディアによると、韓国軍はこの海域に駆逐艦1隻を配備したほか、白●(=領の頁を羽の旧字体に)島と延坪島にも対空ミサイルを増強配備し、北朝鮮の火砲攻撃にも備えているという。

2009年5月19日火曜日

2009年5月17日日曜日

2009年4月12日日曜日

ダー先生

http://www.marmarine.jp/

日本人小学校の恩師が定年後フィリピンのシキホール島に行って開いたペンションです。

みなさま、遠いですが一度行ってみてください。

素晴らしいところだそうです。5年前に同窓会でお会いしましたが相変わらず元気にご活躍していました。全くブレておりません。

日本人小学校の恩師が定年後フィリピンのシキホール島に行って開いたペンションです。

みなさま、遠いですが一度行ってみてください。

素晴らしいところだそうです。5年前に同窓会でお会いしましたが相変わらず元気にご活躍していました。全くブレておりません。

2009年3月15日日曜日

2009年2月23日月曜日

2009年2月17日火曜日

GIC 330億ドルの損失

元本は推定約3000億ドルということなので、約10%の損失となるが、このニュースは先週末よりシンガポールの地場ブログにおいて2000億ドルの損失をしたという話が一人歩きしていたことに対応するためにリークをしたと思われる。実際に、そのような収支になっているかは定かではない。

| Tuesday, 17 February 2009 |

|

|

Costas Paris

Costas Paris2009年2月15日日曜日

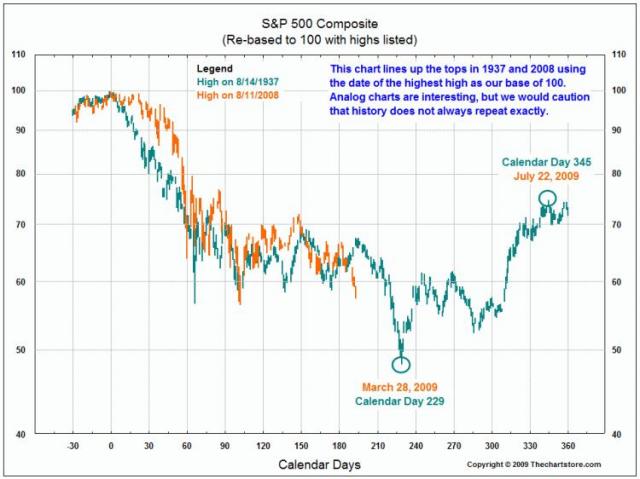

S&Pの予想PERはP/E 58倍らしい

Equity Chart of the Day: S&P Corporate Earnings

Here's a cool S&P earnings chart sourced at Bob Bronson Capital Management.

日本酒醸造元が。。。出来ました!

Hello, Moto

America’s first sake brewpub debuts in Minneapolis

BY Dara Moskowitz Grumdahl

Photo by Terry Brennan

Wine connoisseurship has its dark side: You can devote a decade to the subject and still find yourself at the tip of the iceberg, even after you’ve acquired a financially imprudent fascination with age-worthy Bordeaux. Beer connoisseurship also has its dark side: Go down that path and you will invariably find yourself in the company of people who have strident feelings about shareware. You’ll also end up drinking things that taste like salted, carbonated molasses.

What’s a would-be connoisseur to do? You could become a sake expert—and you could accomplish this with a single visit to Moto-i in south Minneapolis, America’s first and only sake brewpub.

As far as owner Blake Richardson knows, there is only one other sake brewpub in the world, and it is, of course, in Japan. Why is drinking sake that’s brewed on-site a big deal? Because sake is a living, breathing thing—in the same way beer or yogurt is a living thing—and pasteurizing or bottling it to make it shelf-stable and fit for a long journey from Japan to America kills a lot of its flavors and nuances.

What’s that? You didn’t know sake had flavors and nuances? Well, settle in for a quick-course on sake connoisseurship. (I promise it will be quick.)

First, good sake is meant to be served cold. When chilled, the smell of alcohol is tamped down, allowing all sorts of beautiful scents—cucumber, melon, minerals—to emerge. (This is the same reason why wine is supposed to be served at cellar temp-erature; if served too warm, the scent of evaporating alcohol dominates the nose.)

Second, you need to understand that there are only three real variables in sake production: The rice, the yeast, and the water. Sake rice is different from table rice. Each grain is a little heavier and contains a “starch pocket” in its center. Once sake rice is milled to achieve the right ratio of solids to starch, you turn the starch into sugar, which is done with the help of one of the world’s most venerated molds: koji-kin. Then, any one of a number of yeasts turn the sugar into alcohol (just as the sugar in grape juice or beer mash turns into alcohol in wine or beer). Because each of these yeasts creates a slightly different flavor profile, they are very important—so important that at the beginning of the last century, Japanese brewers codified them numerically. Yeast number 7, for instance, is prized for its elegance, while yeast number 14 creates the fragrance of pears and apples.

Water is the final variable. Pure, clean water is utterly necessary for sake, while other elements in the water (minerals and such) impact the yeast and create final flavors.

So, there you go! If you read the above paragraphs and then go and taste one of Moto-i’s sakes, you will be a bona fide sake connoisseur. (Of course, you could go totally nuts and learn the Japanese words for sake-making terms—like nama, for instance, which means unpasteurized—but if you did that you wouldn’t have anything to learn from Moto-i’s lovely place mats.)

Photo by Terry Brennan

And I heartily recommend a trip to Moto-i. In fact, I am adding Moto-i to the list of places you must take visitors when they visit Minneapolis. When you go, you’ll find a large, spare room painted in many wood-colored tones. There are wooden booths, wooden slats covering the windows, and glass screens overhead, topped with long branches and gauzy fabric. Somehow, the overall feeling is one of being in Portland. I don’t know why, other than it seems too spacious to be San Francisco, too dark to be Minneapolis or Los Angeles. So I’m sticking with Portland. When you go, you’ll also find a menu of little bar snacks and casual eats in the model of a Japanese izakaya, a drinking-snack-and-casual-eats bar.

What should you eat at Moto-i? Definitely the house-roasted peanuts, which are complimentary with a full glass of sake (they’re also available on their own). These peanuts, served in their red skins, are roasted with minced Thai chiles and pulverized kaffir-lime leaf, resulting in a smoky, spicy, dusky, devourable little drinking snack. The mussels, steamed in a bit of sake, garlic, and mint, are served with a bowl of rice, like a Japanese versionof the French bistro classic moules frites. A lively little plate of cold soba noodles in a zesty sesame sauce is another treat, and you absolutely shouldn’t miss the rice buns. Each is a sweet, pillowy, admirably tender pancake of rice folded around pickled vegetables and your choice of filling (sweet hoisin pork, less-sweet hoisin chicken, or fried tofu). If you subscribe to the like-goes-with-like wine pairing theory, nothing makes more sense than pairing a rice pancake with a rice beverage. If you subscribe to the all-drinking-goes-well-with-fried-chicken theory, be sure to try the karaage: boneless morsels of soy-marinated chicken dipped in batter and fried till they’re

shatteringly crisp.

Of the big plates, I recommend the truly spicy green coconut curry, with a choice of chicken or mock duck, which adds good flavor to the fire. Of the desserts, the can’t-miss treat is the Okinawan doughnuts: four little piping-hot, fresh-from-the-fryer nuggets of sweet goodness made vaguely Asian by a tiny bit of five-spice powder in their sugar-coating. I defy you not to burn your tongue when presented with hot doughnuts after a night of drinking. I double-dog defy you.

I tried a number of other dishes at Moto-i that left me underwhelmed: unremarkable dumplings, underseasoned ramen, dull Singapore noodles. But even those misses did nothing to diminish my enthusiasm for this utterly novel place. It’s dinner, it’s drinking, it’s smart, it’s inexpensive—what more could you ask from a bar?

Izakayas have been all the rage on the coasts the last few years, and while coast-dwellers get all zany deciding which izakaya is truer to its mission (because it has charcoal grills or whatnot), I really like that we have, in pure Minnesota-eccentric style, leapfrogged ahead of them.

The Minnesota eccentric in question is Richardson, the owner of both the Herkimer brewpub and, now, Moto-i. “When Fuji-Ya opened around the corner from us, I became fascinated with sake,” says Richardson. His idea to open a sake brewpub was only reinforced after a series of trips to Japan, tours of sake breweries, and an apprenticeship at the Japanese sake brewery Momokawa. This led to three years of petitioning the state for permission to open a sake brewery, which he received after cutting though a mountain of red tape. Will Minneapolis fall in love with sake the way Richardson and I have? “A lot of people thought I was crazy to think this would fly here,” Richardson says, “but I studied how much sake people drank in Uptown.” How does one study sake consumption in Uptown? Evidently, you go to Chino Latino, Sushi Tengo, Fuji-Ya, and Azia, and tip well. “I think once people taste the nama-ness, the unpasteurized-ness, the liveliness, the fragrance, the zing, they’ll love it as much as I do,” Richardson says. And they’ll tell their friends in other cities, which will make them jealous. What more could you want in connoisseurship?

Dara Moskowitz Grumdahl is a senior editor at Minnesota Monthly.

Moto-i

2940 Lyndale Ave. S., Minneapolis

612-821-6262

moto-i.com

Lunch and dinner served daily.

2009年1月29日木曜日

ドバイ

http://www.timesonline.co.uk/tol/travel/news/article5607619.ece

開発が急速に進んだために汚物処理を違法投棄する外国人労働者が増え、それが川に流れ込んで海岸を水域を汚染したとのこと。

開発が急速に進んだために汚物処理を違法投棄する外国人労働者が増え、それが川に流れ込んで海岸を水域を汚染したとのこと。

2009年1月26日月曜日

2009年1月4日日曜日

麻生総理大臣 年頭所感

あまり読む方は多くないとは思いますが、このくだりは真理であると思います。

「...私が目指す日本は、「活力」ある日本。「安心」して暮らせる日本です。日本は、これからも、強く明るい国であらねばなりません。

五十年後、百年後の日本が、そして世界が、どうなっているか。未来を予測することは、困難です。

しかし、未来を創るのは、私たち自身です。日本や世界が「どうなるか」ではなく、私たち自身が「どうするか」です。

受け身では、だめです。望むべき未来を切り拓く。そのために、行動を起こさなければなりません。...」

支持率で総理大臣を評価する必要は全くありません。こうした言葉を発することが出来るかどうかが大切であると思います。

「...私が目指す日本は、「活力」ある日本。「安心」して暮らせる日本です。日本は、これからも、強く明るい国であらねばなりません。

五十年後、百年後の日本が、そして世界が、どうなっているか。未来を予測することは、困難です。

しかし、未来を創るのは、私たち自身です。日本や世界が「どうなるか」ではなく、私たち自身が「どうするか」です。

受け身では、だめです。望むべき未来を切り拓く。そのために、行動を起こさなければなりません。...」

支持率で総理大臣を評価する必要は全くありません。こうした言葉を発することが出来るかどうかが大切であると思います。

登録:

投稿 (Atom)